Category: Homeowners insurance

Home insurance prices set to keep rising with severe weather

The average annual premium is projected to increase 4% to about $3,057 this year, after jumping 12% in 2025, according to Insurify, an online insurance comparison site.

Digital claims tools drive property insurance customer satisfaction, JD Power

Customer satisfaction rises in 2026 despite homeowner insurance premiums, according to JD Power’s 2026 property claims satisfaction study.

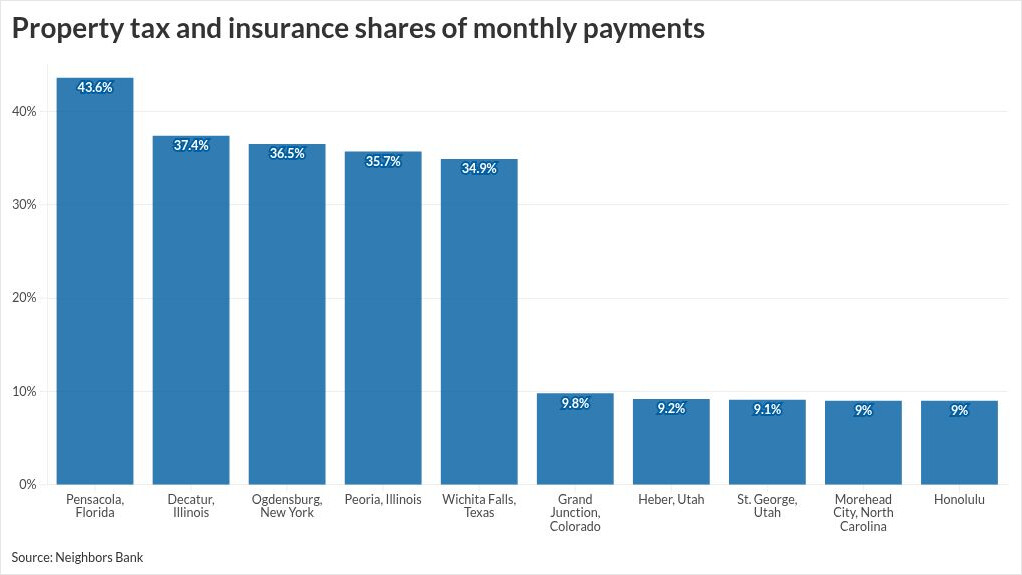

Taxes, insurance eat 21% of mortgage payments

Many homeowners and first-time buyers are surprised by rising property taxes and insurance, which can sharply increase monthly mortgage costs beyond principal and interest.

Trump orders federal takeover of LA wildfire rebuilding efforts

Nearly 40,000 acres were burned in the Eaton and Palisades wildfires last January, killing at least 31 people and destroying 16,000 structures.

Why homeowners insurance rates could stabilize in 2026

Rates actually declined or remained flat over a two-year period in 15 states, including Florida, with natural disasters and tariffs affecting 2026’s movements.

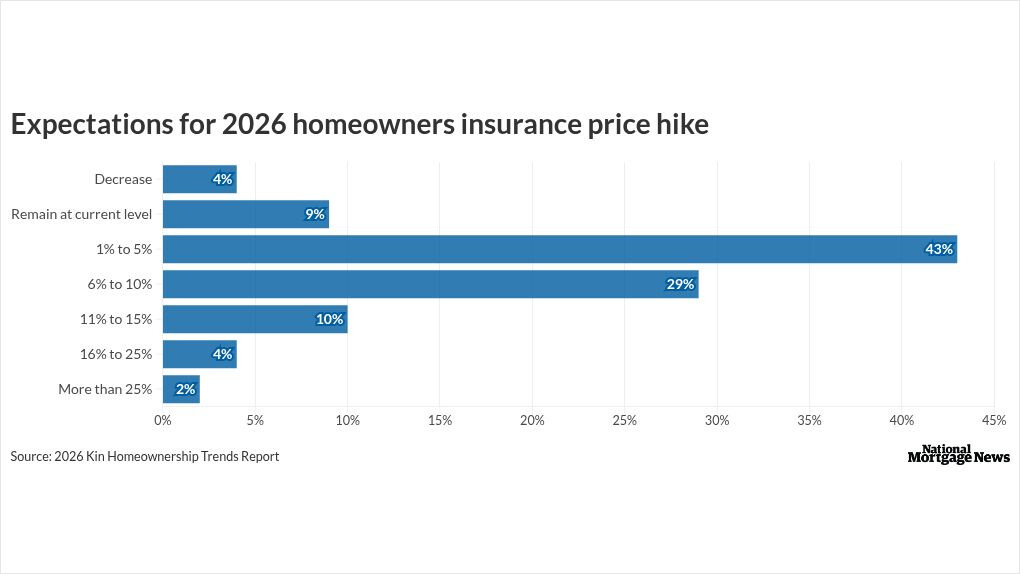

U.S. homeowners expect extreme weather to damage their homes: Kin

U.S. homeowners are concerned about climate and insurance costs, according to Kin’s Homeownership Trends Report.

LA Fire survivors got a rude surprise that could hit more Americans

Since the 1990s, American homes have been systematically underinsured in the event that they are completely destroyed.

Insured losses from wildfires, storms and floods hit record high

Insured losses for so-called non-peak perils — also sometimes referred to as secondary perils — reached a record $98 billion last year, Munich Re said in a report released on Tuesday.

Insurance costs ‘seriously’ influencing many home purchases

The impact of extreme weather remains top of mind for many, with a majority of homeowners citing it as a factor behind purchase or relocation considerations.

US lawmakers launch probe into insurance rating firm in Florida

Three U.S. senators opened an inquiry into insurance ratings firm Demotech and whether its assessments may be exposing taxpayers to growing risks tied to climate-driven insurer failures.